Hey Cool Car Fans,

I have taken a long break from writing at The Cool Car Guy’s Blog. I’ve been crazy busy delivering vehicles to clients over the past couple of years. We moved from Castle Rock, Colorado to Rio Rancho, NM back in April of 2021. We took advantage of the ridiculous home prices caused by inflation to sell our home from COVID-19 like millions of other people around America. CoolCarGuy.com is still in full swing in Lone Tree, CO.

I decided I needed to write an article on the real reason that car prices have gone through the roof since I own a car dealership. Especially, when I hear all of these talking heads on Wall Street trying to tell everyone that this is temporary because of a microchip shortage.

First of all, let’s talk about the fact that traditionally cars are depreciating assets. In a normal economic climate if you buy a new car and drive it about 15,000 miles a year that vehicle is going to drop in value. A vehicle typically depreciates about 30% to 50% over three years. This is how leasing a vehicle works. When you lease, you pay for the depreciation of the vehicle.

Let’s look at a Toyota 4Runner as a real life example. In 2018 a Toyota 4Runner had an original MSRP of $34,810 – $45,160 depending on the trim level and options. An SR5 Premium with 4WD had an MSRP of $36,400. It should sell at auction three years later with 45,000 miles coming off of a lease for about 25% of the MSRP price. This means that it should have depreciated to about $27,300 if it lost 25% of its original value. This is pretty amazing because they hold their value extremely well compared to other vehicles in the marketplace.

Typically, 4Runners depreciate about 25% to 30% over 3 years where many other vehicles depreciate 40% or even 50% of their original MSRP during the same period. If you leased it and drove it 45,000 miles and gave it back to the leasing company at the end of the lease, it should be selling at auction for around $27,300 at the high end in a good market. Is this true after this Covid-19 world that has been created with $5 trillion of money dumped into the economy? Not even close.

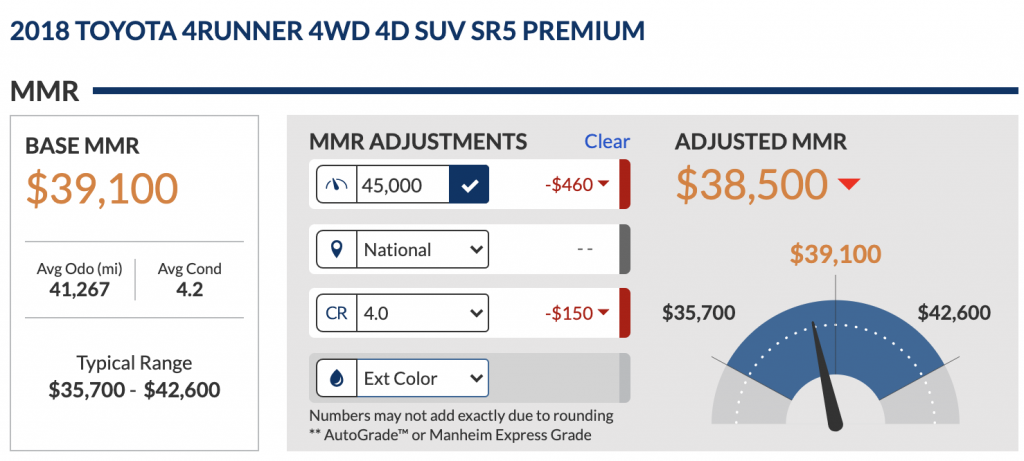

IN JUNE OF 2021, A 2018 TOYOTA RUNNER SR5 PREMIUM IS SELLING AT AUCTION FOR MORE THAN THE ORIGINAL MSRP – SAY WHAT?!

The graphic above is a screenshot of what a 2018 Toyota 4Runner SR5 Premium with an average condition of 4.0 out of 5.0. This vehicle right now is selling for $38,500 minus auction fees. It didn’t depreciate at all in three years, but in fact it appreciated. It is selling for more than the original MSRP, This is not normal by any stretch of the imagination. Which means that if you leased this vehicle, you are in a profit position should you want to get out of it.. Call me if you’re in this situation by the way or you have a leased vehicle before you give it back to the leasing company.

WHAT IS GOING ON AND IS THIS REALLY A MICROCHIP SITUATION LIKE THE MEDIA WANTS EVERYONE TO BELIEVE?

If you turn on the major news programs you will hear their narrative that the problem is primarily supply shortages since the chip manufacturers quit making components. While this is true, let’s put the automobile market in perspective. In 2019, which was before the Covid-19 virus outbreak, automakers sold more than 17 million vehicles in the U.S. for a fifth consecutive year. That seems like a large number of vehicles and it is, but that’s the new car market. There are over 276 million used vehicles in the United States. Did they all disappear?

Of course not. In 2019, the same year that 17 million new vehicles were sold, almost 41 million used vehicles were sold. These used vehicles were not waiting on microchips. The reality is that we are living in an economy with run-a-way inflation.

The Federal Reserve has pumped over $5 trillion into the marketplace. This is causing inflation and they have kept interest rates down, which is driving up the prices of just about everything, including automobiles. They are in a Catch-22 because they can’t tell everyone there is massive inflation and unemployment, even though it’s obvious and you don’t have to read tea leaves to figure it out. They don’t want to create a Wall Street panic and sell off because Capitalism works on consumers buying automobiles, houses, food, etc. Nobody wants to overpay for things and lose money if they have to sell.

Almost 10 million people unemployed, while they are saying that there are 9.4 million jobs. Sure, if you want to go and earn $10 an hour when the average price of a new vehicle is over $40,000 right now. In what world does that work financially? It doesn’t. By shutting down the economy the government stopped a train going 100 miles an hour and the cars in the back are now starting to hit the front of the train. They are trying to convince people that this is just temporary because of the Covid-19 shut downs and it’s all going to come back to normal soon. Maybe in a few years, but you can’t just put the derailed train back on the tracks and keep moving.

You can’t have run away inflation and not have a major increase in wages for the poor and middle class to be able to afford to buy “stuff”. It is economics 101 and any kid who has ran a lemonade stand will understand this. Imagine you pull up to a lemonade stand ran by a 10 year old and you expect to get a cold glass of lemonade for $.50, but to your surprise it’s $10.00, warm and in a dixie cup. You look at the kid and he says, “Sorry but I can’t stand out here all day for fifty cents a glass. You know with the cost of water, ice and lemons these days I have to charge $10 or the math doesn’t work.” Is that a sustainable business or is that lemonade stand going to cease to exist?

Nobody can afford to pay for that kid’s lemonade unless it’s some rich guy in the neighborhood who just wants to give the kid some money each day and buy his lemonade. And these dummies in Washington and at the Federal Reserve are trying to tell everyone that isn’t what’s happening. That’s exactly what is happening. They have pumped $5 trillion into this economy to try to help the kid at the lemonade stand, but it’s not sustainable. They have millions of people getting paid more to stay home than if they worked a job.

The reality is that unemployed people cannot get financed to buy used cars or houses. Millions of people have had their credit destroyed because of the government lock downs, so even if they can get financed it’s going to be at high interest rates. You can’t get a loan if you don’t have a job or bad credit, so these millions of people are not trading out of their vehicles. They can’t. They have to keep them and drive them or pay cash for a vehicle. And that’s why we have a shortage of overprice used vehicles right now. It’s supply and demand for sure, but it’s not just because of missing microchips for new car production. In the words of James Carville in 1992, “It’s the economy stupid”.

_________________________________________________________________________

Auto Consultant – John Boyd: The Cool Car Guy

John is an auto consultant who owns CoolCarGuy.com, a licensed car dealership in Lone Tree, CO. He can help you save time and money on any make or model, new or used, lease or purchase – nationwide! Call or email John about your next vehicle!

jboyd@coolcarguy.com or Twitter @coolcarguy